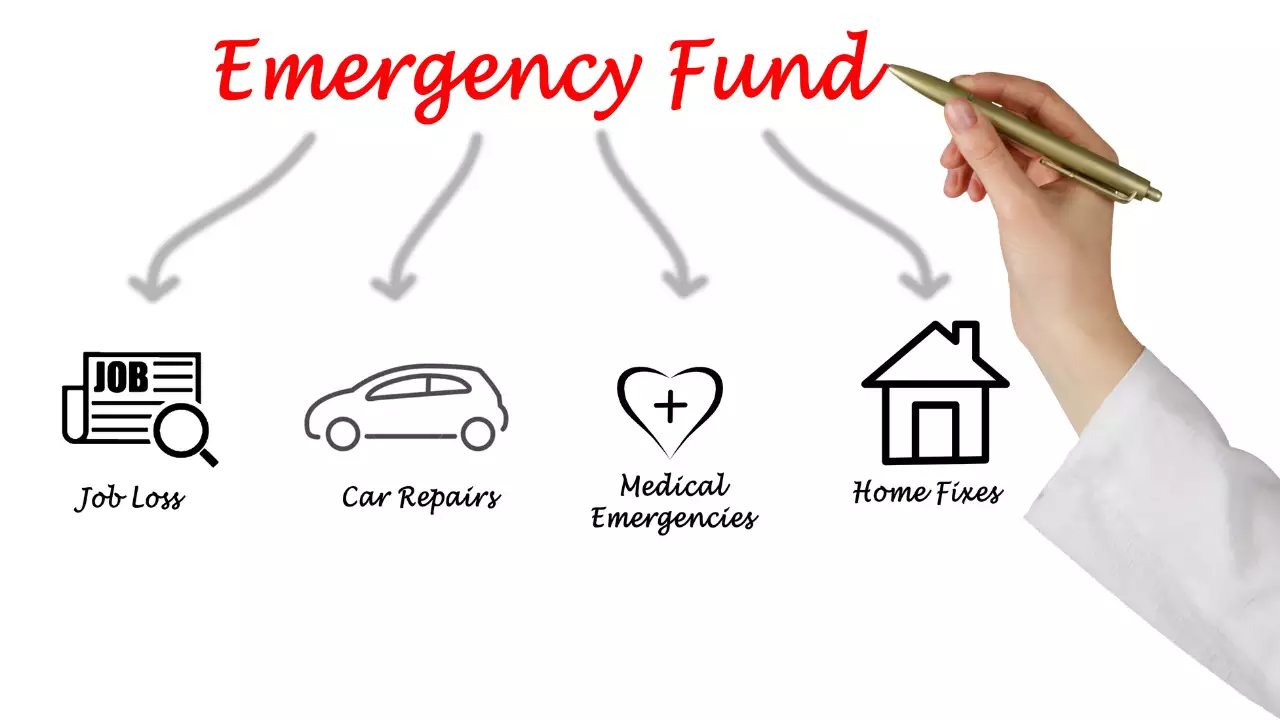

An emergency fund is an essential pillar for achieving financial stability. Having cash savings set aside provides critical protection against sudden income loss, unplanned expenses, and other surprises life may throw at you.

Yet budgeting specifically to build an emergency fund can feel challenging when balancing so many other financial priorities too.

This comprehensive guide explores straightforward strategies for budgeting to create your emergency cash reserves. Whether currently living paycheck-to-paycheck or enjoying a comfortable salary, a few adjustments make all the difference in designating this safety net priority.

Follow these steps to craft a budget allowing growing emergency savings goals steadily over time – no matter what crisis hits next.

Step 1: Set Your Emergency Fund Savings Goal

Know exactly how much you should aim to set aside in easily accessible savings to cover emergency costs. Financial experts typically recommend having enough to cover:

3-6 Month’s Worth of Essential Expenses

Add up recurring necessities like rent/mortgage, groceries, utilities, insurance, medication. Multiply by three to six months as your savings goal. This protects losing a job or income stream for that period while finding alternatives.

For example, if your rent, food, and transport costs around $1,500 monthly, aim for $4,500 to $9,000 in emergency savings to remain supported for 3-6 months if made redundant.

Of course, determine the exact goal based on your household’s unique situation and risk comfort levels. Having over 6 months of expenses covered brings extra reassurance. Or if your income fluctuates anyway, storing just a few thousand dollars might bridge gaps between pay cycles.

Anticipated Irregular Expenses

Also factor savings necessary for hitting foreseeable big ticket expenses occasionally falling due over 1-2 years. These might include:

- Insurance deductibles – e.g. $500 for your car

- Medical or dental costs – e.g. $3,000 for orthodontic treatment

- Car repairs – e.g. $1,000 for engine overhaul

- Annual bills – e.g. $600 in property taxes

Totaling these predicted lumpy costs reaching a few thousand dollars over a couple of years provides a sensible addition to emergency fund goals. This readies available cash when one-off but inevitable payments arise unexpectedly.

Once defining your emergency savings target – whether $5,000, $15,000 or more – making steady progress towards this through an allocated budget becomes essential.

Step 2: Cut Existing Expenses Where Possible

Freeing up cash to redirect towards emergency savings begins by reducing lower priority current spending. Analyzing recent bank statements exposes possibilities like:

Trimming Variable Costs

- Downgrade unlimited mobile data plans to cheaper limited data options

- Eat out for dinner twice monthly rather than weekly

- Walk places under 5km rather than frequently driving

Small cutbacks on flexible spending quickly compound monthly savings easily divertible straight to emergency funds goals.

Canceling Unnecessary Subscriptions

- Music or video streaming services barely used

- Specialty apparel boxes, food crates, beauty boxes

- Memberships to clubs no longer attended

Removing wasted subscriptions generates substantial savings from monthly budgets. When I checked, I found myself to be subscribed to 3 video/movie streaming services which I haven’t used in months!

Temporarily Pausing Financial Commitments

Halting some savings top-ups short-term while redirecting those funds to urgent emergency fund priorities:

- Reduce additional mortgage repayments

- Lower voluntary superannuation (retirement) account contributions

- Pause college savings contributions for young kids

There’s opportunity to restart other less crucial financial goals later. Yet guaranteeing emergency savings comes first.

With numerous areas typically allowing reduced expenditures, allocate these newfound amounts for expanding emergency reserves right away.

Step 3: Welcome New Income Directly Into Savings

As well as cutting current costs to inject savings, automatically dedicating any new or unexpected income gains directly into emergency funds accelerates reaching goals faster.

Savings Strategies For Common Income Boosts:

Tax Refunds – Forward the full lump sum amount upon receiving annual tax refund rather than tempting splurges.

Work Bonuses – Like tax returns, resist viewing bonuses or commissions as just more spending money. Prioritize emergency savings instead.

Gift Money – Whether $50 from a grandparent or $500 birthday cheque from parents, bank the funds.

Sold Assets – Clothes, jewelry, electronics, or furniture no longer used could be worth hundreds of dollars. Pass sale proceeds straight into savings.

Income Increases – Promotions and pay rises offer an obvious chance for emergency fund contributions. Upon salary increasing $200 monthly, for example, immediately allocate this full extra portion into savings rather than lifestyle inflation.

By leveraging whatever surprise money comes your way expressly for emergency purposes, you rapidly reach safety net goals seemingly distant if only relying on tiny redirected amounts scraped from everyday budgets.

Step 4: Make Saving Automatic

The biggest obstacle to successfully growing emergency funds through a budget involves tempting discretionary spending eroding those savings goals. A $100 clothing purchase here, $200 there on a weekend getaway rapidly diminishes an account balance you worked hard designating for other important purposes.

The simple yet highly effective solution making emergency fund savings foolproof includes:

Automate Contributions

Arrange scheduled automatic transfers from your everyday spending account into a dedicated high interest emergency fund savings account. Set up fortnightly or monthly deposits mirroring pay cycles – allowing spending from one account while growing the other untouched.

Make Contributions Invisible

Further limit spending temptation from your nominated emergency savings by holding this money in a totally separate account, possibly even an alternative bank. This also heightens mental separation between everyday “fun money” versus untouchable reserves kept for true emergencies only.

Removing manual effort to make contributions combined with hiding those growing balances from ready access trains spending habits to ignore these amounts entirely. Your hands are forced to let emergency savings remain an automated untouchable pot continuing growing.

Step 5: Strategically Withdraw Funds When Vital

Despite temptations along the way, celebrate finally reaching your full emergency savings target! Pat yourself on the back knowing this financial safety net protects against whatever happens next needing cash quickly.

Then if faced with a sudden major expense like urgent medical bills, emergency car repairs, or an unexpected job loss, now’s the time to gratefully unlock those savings supporting you through the crisis.

However, Remember To:

- Only withdraw enough to cover true essentials – don’t see it as “free money” paying for luxuries like vacations or home renovations.

- Track spending from the account – log where every dollar goes returning later if required for insurance claims.

- Aggressively replenish after using funds – resurrect savings habits returning balance to full prior levels before entertaining other ambitions again.

Treating emergency savings reserves both cautiously and intentionally ensures they repeatedly come to your aid whenever genuinely needing immediate financial help.

Step 6: Budget Ongoing Contributions

Rebuilding emergency savings after strategically withdrawing funds requires recommitting to consistent ongoing budgeted contributions until reaching your original savings target again.

Ideas For Budgeting More Into Depleted Emergency Funds:

- Divert annual pay rises or bonuses straight back into savings

- Save intermittent windfalls like tax refunds or workplace incentives

- Apply side hustle income specifically towards replenishing reserves

- Raise automatic monthly deposits to higher levels

- Further trim discretionary spending from everyday budgets

Diligently funneling multiple cash inflows towards bringing that emergency fund balance back to the necessary level for your household’s risk tolerance reinstates this vital backup support.

Conclusion: Consistency Is Key

Committing to consistently budgeting portions of income into an emergency savings fund seems challenging juggling so many near-term spending priorities too. But by cutting flexible costs, harnessing windfalls, and saving automatically over time, your emergency reserves grow in the background ready whenever fate strikes.

Use the steps outlined here to instill designated emergency fund contributions into your regular household budget today. Growing this backup financial security blanket repays exponentially whenever you inevitably need support.

Stay disciplined designating small pockets of money aside each month. Celebrate inching closer towards your end emergency savings goals bringing confidence to handle life’s unexpected curveballs thrown your way anytime.

{kind=link}